Buying insurance once felt to me like prepping for a zombie apocalypse—everyone said it was essential, yet every policy looked suspiciously vague. I even picked my first auto plan because of a cartoon lizard. Spoiler: it wasn’t the best move. This insurance coverage guide is the candid, practical walkthrough I wish I’d had—so you can choose confidently, skip the traps, and protect what matters without overpaying.

For a broader roadmap that fits this goal into your whole money picture, see this practical companion: Personal Finance Guide.

Table of Contents

Your Insurance Coverage Guide: The Big Picture

Insurance isn’t exciting, but it is the quiet backbone of a strong financial plan. One ER visit, fender-bender, kitchen fire, or untimely loss can wipe out savings. The right coverage turns worst-case scenarios into manageable hiccups.

Here’s the sweet spot: enough protection to cap your downside—without bloated premiums. This insurance coverage guide breaks down health, auto, life, and homeowners insurance, explains key trade-offs, and shows how to compare providers wisely.

Four Essentials You Shouldn’t Ignore

- Health insurance: Helps cover major medical costs, prescriptions, and preventive care—critical in the U.S.

- Life insurance: Creates a financial safety net for dependents—kids, spouses, even aging parents.

- Auto insurance: Required in almost every state; protects you after accidents, theft, or lawsuits.

- Homeowners insurance: Shields your biggest asset (and your liability) when the unexpected strikes.

Health Insurance: What to Get and What to Skip

I once chose the cheapest Bronze Marketplace plan because “I’m healthy.” Then a running injury sent bills the size of a used car. Lesson learned.

Where to buy

- Employer plans (most common for working Americans)

- Healthcare.gov Marketplace (for individuals/families)

- Medicaid (income-based)

- Medicare (65+ or certain disabilities)

For official plan details and enrollment windows, visit Healthcare.gov

Key terms, decoded

- Premium: Your monthly payment.

- Deductible: What you pay before insurance pays.

- Copay: Fixed fee for a visit or service.

- Out-of-pocket max: After you hit this amount in a year, the plan pays 100% of covered services.

Network types

- HMO: Lower cost, smaller network; referrals required.

- PPO: Higher cost; more freedom to see out-of-network providers.

- EPO: No referrals; in-network only.

- HDHP: High deductible; HSA-eligible.

Metal tiers (ACA plans)

- Bronze: Lowest premiums, highest out-of-pocket.

- Silver: Middle ground; eligible for cost-sharing reductions if you qualify.

- Gold/Platinum: Higher premiums, lower out-of-pocket.

Must-haves vs. nice-to-haves

Must-haves:

- Your preferred doctors/facilities in-network

- Mental health coverage and preventive visits

- Prescription coverage that matches your meds

Nice-to-haves:

- Vision/dental add-ons

- Telehealth (often included now)

- Wellness benefits (gym credits, programs)

Smart cost moves

- Use an HSA with an HDHP to pay qualified expenses with pre-tax dollars.

- If offered, use an FSA for predictable costs, and watch “use-it-or-lose-it” rules.

- Stay in-network whenever possible.

- Check prescriptions on the plan’s formulary before enrolling.

Example: Freelancing, I paired a high-deductible plan with an HSA to save on taxes. Later, a job with a PPO made sense for broader access and fewer surprise bills.

Quick Tip: Before booking care, verify “in-network” with your insurer’s directory or by calling the clinic—never just assume.

Life Insurance: Practical Protection for People You Love

I thought life insurance was only for “older” people—until I realized my student loans and family responsibilities didn’t vanish if I did.

Term vs. permanent

- Term life: Coverage for 10, 20, or 30 years. Affordable. If you pass during the term, your beneficiaries receive the benefit.

- Whole life (and universal): Lifetime coverage, often with cash value. Useful for specific planning needs but pricier.

How much coverage?

A quick rule: 7–10x your annual income plus major debts and goals (mortgage, child care, tuition). Adjust for your situation, especially if you’re single with no dependents.

Example: A healthy 35-year-old non-smoker can often get a $500,000, 20-year term policy for well under $40/month (quotes vary by health and insurer).

Helpful add-ons (riders)

- Accelerated death benefit

- Waiver of premium (if you become disabled)

- Child term rider

Due diligence: Check an insurer’s complaint trends and consumer resources via the NAIC. A rock-bottom premium isn’t worth sluggish or disputed claims.

Auto Insurance: Get the Right Limits, Not Just the Lowest Price

Auto coverage is required in nearly every state. At minimum, you need liability insurance (injuries and property damage you cause others). Most drivers add:

- Collision: Repairs your car after a crash.

- Comprehensive: Theft, vandalism, storms, falling trees, animal strikes.

- Uninsured/Underinsured Motorist (UM/UIM): Protects you if the other driver is underinsured or uninsured.

- Medical payments or PIP (varies by state): Helps pay medical bills for you/your passengers.

Real life: When I drove an old beater, I skipped collision. After upgrading, I added collision and comprehensive—and was grateful when a storm sent a branch through my windshield.

Choosing liability limits

State minimums are often too low. Consider 100/300/100 ($100k per person, $300k per accident, $100k property), or higher if you have assets to protect.

What affects your premium

- Driving record, age, credit, vehicle model

- State and ZIP code (urban areas tend to be pricier)

- Discounts: bundling, telematics/safe driving apps, low mileage, student, multi-car

For vehicle safety insights, visit NHTSA or the Insurance Information Institute.

Cost savers: Compare quotes yearly, raise deductibles if you can handle a larger out-of-pocket cost, and ask about every discount you might qualify for.

Homeowners Insurance: Protect Your Biggest Asset

Buying my first home in tornado country taught me that details matter.

What’s usually covered

- Dwelling and other structures (garages, fences)

- Personal property (your stuff)

- Loss of use (hotel/meals if you can’t live at home temporarily)

- Personal liability (injuries on your property or damage you cause)

What’s not covered by default

- Floods (separate policy via the National Flood Insurance Program or private market)

- Earthquakes (separate coverage)

- Wear and tear, maintenance issues

Check your flood risk and options at FloodSmart.gov

Coverage amount and valuation

- Insure at replacement cost (what it costs to rebuild), not market value.

- Inventory your belongings and consider replacement cost for personal property.

- Watch for special limits on jewelry, art, and electronics; schedule high-value items.

Real life: A neighbor assumed his standard policy covered basement flooding. It didn’t. The extra flood policy would’ve cost less than a monthly latte habit.

Geography matters

- Gulf Coast, Midwest: Flood risks—consider NFIP or private flood policies.

- West: Wildfire exclusions/deductibles are evolving; verify what’s covered.

- Tornado/Coastal areas: Wind/hurricane deductibles may apply.

Compare Providers with a Clear System (Not Just Price)

The cheapest premium is rarely the best deal. Compare apples-to-apples limits and deductibles across companies, then look at service quality.

How to vet insurers

- Complaint trends and consumer guides: NAIC (https://content.naic.org/consumer)

- Satisfaction studies: J.D. Power (search by line of insurance)

- Financial strength ratings: AM Best and other rating agencies

Red flags

- Lots of exclusions buried in fine print

- High complaint ratios, slow claims

- Hard-to-reach or unhelpful customer support

Power move: Keep a shortlist of two to three trusted carriers for each policy type. That way, you can swap at renewal without starting from scratch.

The Claims Process—Make It Painless

Filing a claim doesn’t have to be a horror story. Preparation helps.

- Health: Call your insurer and provider, file required forms promptly, and keep explanation of benefits (EOBs) and receipts.

- Auto: Document the scene, record witness info, file a police report if needed, and notify your insurer quickly.

- Life: Beneficiary contacts the insurer, submits the death certificate, and completes claim forms.

- Homeowners: Take photos/videos, protect from further damage, keep receipts, and report promptly.

Pro Tip: Store digital copies of policies, IDs, photos of valuables, and contact numbers in cloud storage. It’s a lifesaver when stress is high.

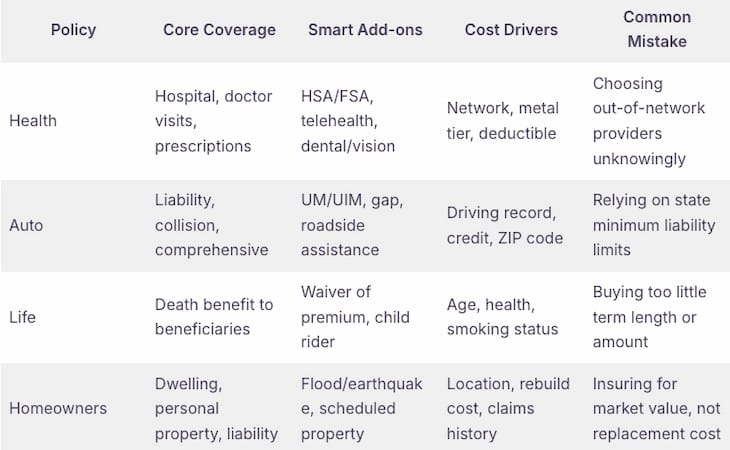

Quick Comparison Table

When to Update Your Policies

- New job or benefits change (health networks and costs)

- Marriage, divorce, or a new child (life insurance beneficiaries and amounts)

- Move to a new state or neighborhood (auto and home rating changes)

- Major purchases/renovations (home coverage and scheduled items)

- Paid off a car or changed its use (auto coverages and deductibles)

Actionable Ways to Cut Costs—Without Cutting Protection

- Bundle home and auto where it truly saves you.

- Raise deductibles if you have an emergency fund.

- Use usage-based auto programs if you’re a safe, low-mileage driver.

- Shop your rates at renewal—don’t auto-renew blindly.

- Ask about loyalty, good driver, student, defensive driving, and paid-in-full discounts.

- For health, verify prescriptions are on the plan formulary, and use in-network providers.

- For homeowners, install smoke detectors, water sensors, and security systems for potential discounts.

How This Insurance Coverage Guide Helps You Choose

This insurance coverage guide is built to shortcut the learning curve. It blends practical definitions, real-life examples, and credible resources so you can compare confidently and avoid unpleasant surprises.

Your 12-Point Confidence Checklist

1) List what you’re protecting (income, home, car, dependents).

2) Decide your budget and risk tolerance (deductibles vs. premiums).

3) For health, confirm your doctors and prescriptions are covered.

4) Use HSAs/FSAs where they truly benefit you.

5) For auto, choose liability limits that actually protect your assets.

6) Consider UM/UIM coverage—it’s often overlooked and invaluable.

7) For life, choose a term long enough to cover your biggest obligations.

8) Vet insurers using NAIC complaint data and satisfaction ratings.

9) Insure your home at replacement cost; schedule valuable items.

10) Add flood coverage if your risk is anything above minimal.

11) Compare quotes yearly and after major life changes.

12) Keep a digital claims kit: policies, photos, receipts, contacts.

Final Word

You don’t need to memorize insurance jargon to make good choices. Focus on the essentials, compare like a pro, and adjust as your life evolves. Protect what matters, skip the fluff, and keep your money working for you.

If you’ve got a win, a cautionary tale, or a head-scratcher, drop it in the comments. I’m still learning too—just a curious soul on a financial journey. Stay curious, stay covered.

External resources mentioned in this insurance coverage guide :

- Healthcare.gov for official plan info: https://www.healthcare.gov

- NAIC consumer tools and complaint data: https://content.naic.org/consumer

- Vehicle safety and auto resources: https://www.iii.org/ and https://www.nhtsa.gov/