If you only think about taxes between January and April, you’re likely leaving money on the table. Midyear tax planning gives you time to make calm, deliberate adjustments that can lower your this year’s tax bill, increase your refund, and help you avoid last‑minute stress.

As a practical rule, midyear tax planning works best when you review your income, withholdings, and deductions while there’s still time to act. The changes you make now can compound—through smarter contributions, better documentation, and strategic timing—by the time you file next spring.

In this guide, I’ll walk you through the most useful midyear tax planning moves for this year, including how to adjust withholding, maximise pre‑tax savings, avoid penalties if you’re self‑employed, and manage charitable gifts and capital gains wisely.

If you’re building a broader money plan, you’ll also find this helpful: a comprehensive personal finance guide that connects credit to budgeting, debt payoff, and long-term goals.

Table of Contents

The Tax Landscape at a Glance

Midyear is the perfect moment to align your plan with current rules.

- Standard deduction (Single): $14,950

- Standard deduction (Married filing jointly): $29,900

- 401(k)/403(b) contribution limit: $23,500 (+$7,500 catch-up for 50+)

- IRA contribution limit: $7,000 ($8,000 if 50+)

- HSA contribution limit: $4,300 individual; $8,550 family (+$1,000 catch‑up for 55+)

Tax brackets are adjusted for inflation, which may gently lower your effective rate if your income hasn’t jumped. The Child Tax Credit remains up to $2,000 per qualifying child (with up to $1,600 refundable), subject to the usual phaseouts.

Tip: Always verify current-year limits on IRS.gov before you act. Rules change, and midyear tax planning is most effective when you’re using the latest figures.

What Is Midyear Tax Planning—and Why It Matters

Midyear tax planning is simply taking stock of your year-to-date income, withholding, and deductions—then making deliberate tweaks before December 31. It’s not flashy; it’s effective. By reviewing now, you can still adjust payroll withholding, step up retirement or HSA contributions, time charitable gifts, and shape how much you’ll owe (or get back) at filing.

A quick example: If your refund was huge last year, you likely overpaid through withholding. Revisiting your W‑4 now can give you slightly bigger paychecks the rest of the year—and still keep your tax outcome steady. That’s the quiet power of midyear tax planning.

Adjust Your Withholding Before It’s Too Late

If you received an unexpectedly large refund, you gave the government an interest‑free loan. If you owed a surprise balance, your withholding was too low. Midyear tax planning fixes both.

Action steps:

- Use the IRS Tax Withholding Estimator to check your current withholding against projected income: https://www.irs.gov/individuals/tax-withholding-estimator

- Submit an updated Form W‑4 to your employer if the estimator suggests adjustments.

- Revisit after major life events (marriage, birth, new job, side income).

Penalty protection: To avoid underpayment penalties, aim to meet a “safe harbor.” In most cases, that means paying in at least 90% of your current‑year tax or 100% of last year’s tax (110% if your adjusted gross income exceeded $150,000).

Midyear bonus: Making a small withholding change now spreads the impact over multiple paychecks, so your take‑home pay doesn’t swing wildly.

Maximize Pre‑Tax Contributions (While There’s Time to Compound)

One of the most reliable midyear tax planning wins is to increase contributions to pre‑tax accounts. Every dollar can reduce your taxable income.

- 401(k) or 403(b): For this year, you can contribute up to $23,500, plus a $7,500 catch‑up if you’re 50 or older. Ask HR to raise your deferral percentage now. Investing earlier means more months in the market.

- Traditional IRA: Contribute up to $7,000 ($8,000 if 50+). Deductibility depends on income and workplace plan coverage, but even non‑deductible contributions may make sense for long‑term growth.

- Health Savings Account (HSA): If you have an HSA‑eligible high‑deductible health plan, limits are $4,300 for individuals and $8,550 for families, plus $1,000 catch‑up for 55+. HSAs offer a rare triple tax benefit: tax‑deductible contributions, tax‑free growth, and tax‑free withdrawals for qualified medical expenses.

- Flexible Spending Account (FSA): FSAs are use‑it‑or‑lose‑it (with limited carryover or grace periods). Midyear is a good time to reassess your election if you have a qualifying life event.

Pro move: Automate monthly or per‑paycheck increases. It eases cash flow and keeps your midyear tax planning on track.

Self‑Employed or Side Hustling? Don’t Miss Estimated Taxes

If you freelance, consult, or drive significant gig income, midyear tax planning means staying ahead of estimated taxes.

- Check Next quarterly deadline

- Avoid penalties by meeting safe harbor thresholds (see Publication 505). Many self‑employed taxpayers set aside 25–30% of net income for federal taxes as a starting point, then refine with a tax pro.

- Track every deductible expense: mileage, home office, software, supplies, contractor payments, and health insurance premiums if you qualify. The simplified home office method allows $5 per square foot (up to 300 square feet) in lieu of actual expenses.

- 1099‑K awareness: Platforms like PayPal, Venmo, and eBay issue Form 1099‑K once you exceed the annual threshold. This year, more payments are being tracked.

Good records are everything. Use a bookkeeping app, keep mileage logs current, and store receipts digitally so you aren’t scrambling in March.

Make Charitable Contributions Work Harder

Charitable giving is meaningful—and with thoughtful midyear tax planning, it can also be tax‑smart.

- Donate appreciated stock instead of cash. You may avoid capital gains tax and still deduct the full fair market value if you itemize and meet AGI limits.

- “Bunch” donations in one year. If you usually take the standard deduction, consider grouping two years of giving into one year to exceed the standard deduction and itemize; use a donor‑advised fund to pre‑fund future gifts while taking a current‑year deduction.

- Documentation matters. For any single contribution of $250 or more, you need a contemporaneous written acknowledgment from the charity. Non‑cash donations over $500 require Form 8283.

- AGI limits: Cash gifts to public charities are generally deductible up to 60% of AGI; appreciated assets to public charities are typically capped at 30% of AGI.

Retiree note: If you’re age 70½ or older, consider a qualified charitable distribution (QCD) from an IRA. A QCD can satisfy part or all of your required minimum distribution (RMD) and keep the amount out of taxable income.

Manage Capital Gains Before They Sneak Up

Market gains realized now are taxable next spring. Midyear tax planning helps you steer the outcome.

- Tax‑loss harvesting: If you have positions below your cost basis, you can sell to realize a capital loss and offset gains. Be mindful of the wash‑sale rule: repurchasing a substantially identical security within 30 days of the sale disallows the loss.

- Long‑term vs. short‑term: Hold investments for more than a year to aim for lower long‑term capital gains rates.

- Asset location: When possible, place income‑heavy assets (like bond funds) in tax‑advantaged accounts and tax‑efficient assets (like index ETFs) in taxable accounts.

Example: Suppose you realized $6,000 in mutual fund gains earlier this year. Harvesting $4,000 in losses from a lagging position can offset most of the tax, and you can reposition into a similar—but not substantially identical—holding to maintain your strategy.

Recordkeeping: Your Built‑In Audit Insurance

Audits are uncommon, but documentation is non‑negotiable. Strong records make midyear tax planning stick.

- Store receipts digitally, back them up in the cloud, and organize by category.

- Keep tax records at least three years; keep basis and closing documents for property and investments until three years after you sell.

- For self‑employed filers, preserve mileage logs, invoices, 1099s, bank statements, and payroll reports.

A clean paper trail is the difference between a deduction allowed and a deduction lost.

Midyear Tax Planning Checklist

- [ ] Adjust your W‑4 using the IRS estimator to prevent surprises.

- [ ] Increase retirement plan and HSA contributions; automate if possible.

- [ ] If self‑employed, prepare for the September 15 estimated tax deadline.

- [ ] Plan charitable giving; consider appreciated assets or donor‑advised funds.

- [ ] Review capital gains and losses; harvest strategically and avoid wash sales.

- [ ] Organize and back up receipts and logs.

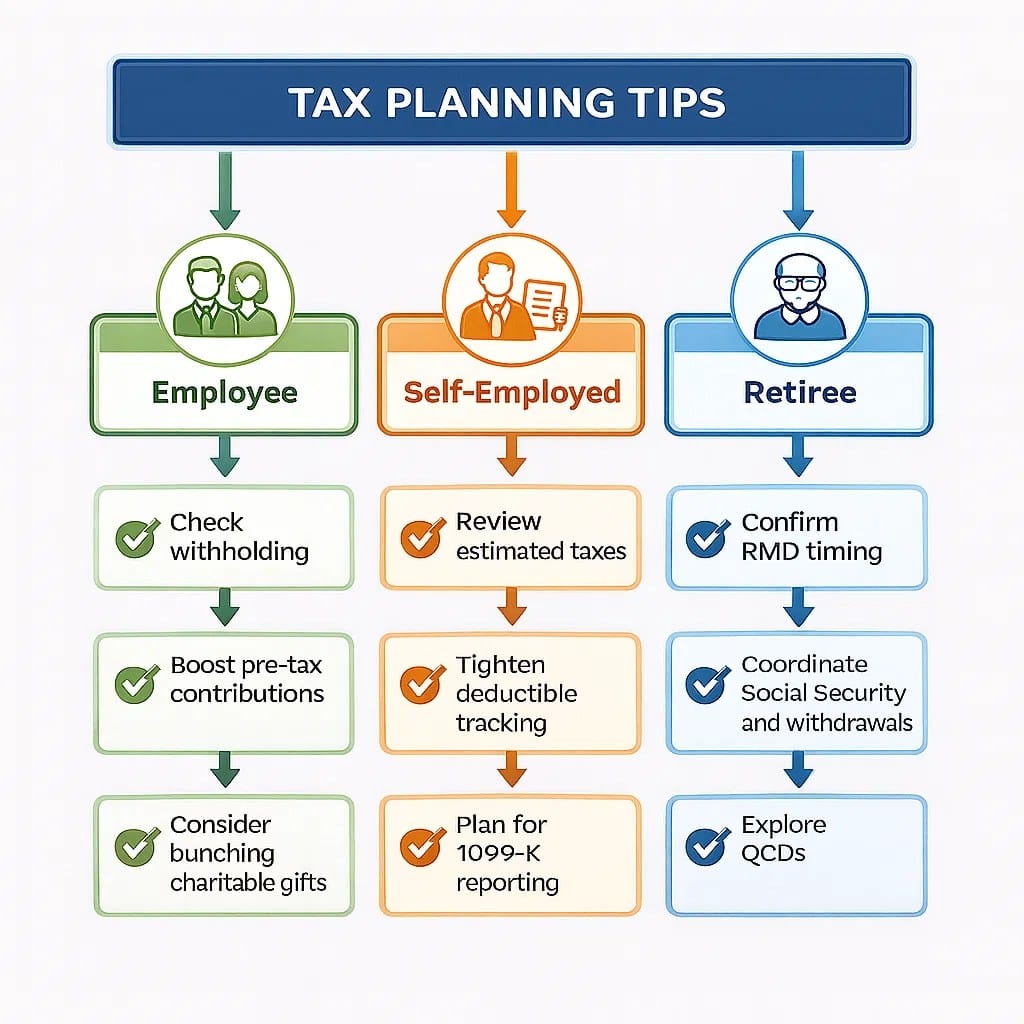

Quick Flow: Choose Your Path

- Employee: Check withholding → Boost pre‑tax contributions → Consider bunching charitable gifts.

- Self‑Employed: Review estimated taxes → Tighten deductible tracking → Plan for 1099‑K reporting.

- Retiree: Confirm RMD timing → Coordinate Social Security and withdrawals → Explore QCDs.

Quick Reference to Limits

| Category | Limits / Dates |

|---|---|

| Standard Deduction (Single) | $14,950 |

| Standard Deduction (Married Filing Jointly) | $29,900 |

| 401(k)/403(b) Contribution | $23,500 (+$7,500 catch‑up 50+) |

| IRA Contribution | $7,000 (+$1,000 catch‑up 50+) |

| HSA Contribution | $4,300 individual; $8,550 family (+$1,000 catch‑up 55+) |

Note: Confirm the latest limits and deadlines on IRS.gov, as updates can occur.

Practical Midyear Scenarios (And What to Do)

- Paycheck spike from a bonus? Use the withholding estimator and nudge your W‑4 to avoid a year‑end bill.

- New side income? Start a separate tax savings account and sweep in 25–30% of net income weekly. Re‑check safe harbor targets quarterly.

- Sitting on appreciated stock? Consider donating shares you’ve held more than a year to a donor‑advised fund this year and recommend grants over time.

- High medical bills? If you have an HSA, increase contributions now to pay current or future qualified expenses tax‑free.

These are the kinds of targeted, real‑world decisions that make midyear tax planning pay off.

Frequently Asked Questions

Is it too late in the year to change my withholding?

No—adjusting in late summer or early fall is ideal. You still have multiple pay periods to spread changes smoothly across your remaining paychecks.

How many times can I update my W‑4?

As needed. Most employers will process a new W‑4 within one or two pay cycles. Use the IRS estimator to avoid guesswork.

Should I prioritize 401(k) or HSA contributions?

If you’re HSA‑eligible, the HSA’s triple tax benefit is hard to beat, especially if you expect medical costs. Otherwise, contribute enough to your 401(k) to capture the full employer match, then consider the HSA and additional retirement contributions.

What if I can’t itemize this year—do charitable gifts still help?

If you take the standard deduction, you won’t get an additional deduction for gifts. Bunching donations into a single year (often via a donor‑advised fund) can help you itemize in that year and still meet your giving goals.

The Bottom Line

Midyear tax planning is quiet, steady, and powerful. With a few timely adjustments—tuning your withholding, boosting pre‑tax savings, planning charitable donations, managing gains and losses, and tightening your records—you can lock in savings, minimize penalties, and enter 2026 with confidence.

Start now. The tax outcome you want next spring is built with the choices you make today.